Despite the good intentions of the government, Georgia’s pension reforms are doomed to failure.

In July, Georgia’s parliament approved a long-overdue new pension law. But these reforms will not fulfil their main purpose — to significantly increase pensions for citizens retiring in the coming years.

In a country where incomes are low and unequally distributed and informal labour is rampant a saving pension scheme such as this will change nothing for the most Georgians.

Back-door reforms

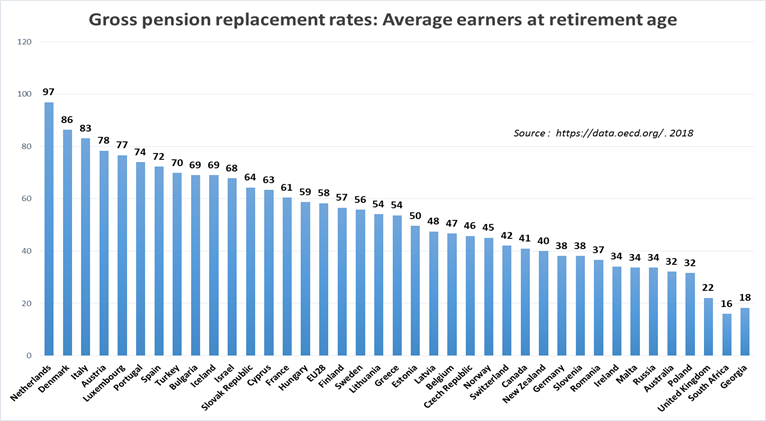

Despite this year’s budget raising the basic pension by ₾20 ($7) per month, the increased pension of ₾200 ($73) will remain one of the lowest in the world. It will equal just 18% of the average wage in the country (the pension replacement rate); by comparison, the average for EU countries is 58%.

This made the pension reforms probably the most important law to be passed after the adoption of a new constitution, but they have not been followed by public hearings or broader informational campaigns.

According to a 2017 survey by the Friedrich Ebert Foundation, less than 2% of respondents considered themselves fully informed about the reforms; 53% had not heard of them at all. An NDI survey conducted after the law was approved showed similar results.

This is no accident. Because the reforms are not designed to increase pensions in the medium term, public debates would certainly be a challenge for the government.

Introducing these reforms by the back door may have postponed public resistance for now, but as the reform lacks popular legitimacy, this will certainly erupt in the future — presumably when the first generation of participants of the scheme retire.

What’s in the reform?

• Employees given personal pension account under the Pension Agency.

• Employers, employees, and the government each contribute 2% of an employees salary.

• The Pension Agency manages and invests the savings with returns accrued in the personal pension accounts.

• Every employed man under 60 and woman under 55 automatically enrolled.

• Those older than 40 can withdraw if they choose.

• Self-employed people can participate voluntary but need to formalise their labour and pay 4% of their income; the government will add 2%.

• Upon retirement, pensioners can withdraw the entire sum or distribute it over their remaining years based on average life expectancy in the country.

Who will be excluded — the failure of the reform

The Government has touted the reform as crucial for business, as it will create ‘long-term money’ and increase credit availability in the country. According to Deputy Finance Minister Nikoloz Gagua, the pension reform is being implemented exactly for the business sector.

But for Georgia’s future pensioners, this will be of little consolation.

One of the key criteria for a successful pension scheme based on contributions is coverage of the population. According to 2017 data from Geostat, more than half of all employees in Georgia — over 880,000 people — are self-employed.

As in most developing countries, most of these people, 83% of them, are engaged in subsistence agriculture, where productivity is very low. In 2017, only 8.2% of total economic wealth (GDP) was produced in agriculture, despite 43% of the total workforce being employed in the sector.

It’s clear that most self-employed people will not voluntarily enrol in this pension scheme since they are the working poor and for them, today’s consumption (without saving for a pension) is a question of survival.

Moreover, for most self-employed people, formalising their labour, a requirement for the new scheme, would mean a substantial reduction of their already low incomes. This would mean paying a 20% income tax together with the pension contributions, and clearly, the state’s 2% co-financing has no chance of tempting many.

Even if all employed people over 40 stay in the pension scheme, an unlikely prospect, more than half of the workforce, the self-employed, will still be left out.

Lifelong inequality

For those retiring in the coming years, these reforms will be almost equally as useless.

According to the Ministry of Economy, the number of pensioners will reach 1 million by 2039, meaning at least 35,000 people will retire annually.

The average salary for people close to retirement is almost half the national average. As salaries start to decrease after peaking in middle age, we should not expect these people to earn enough to accumulate in a savings scheme.

For the pensions of an average earner to be at least ₾100 ($37), a minimum 10–15 years saving period is needed. This means that tens of thousands of people who retire in the coming years will be almost entirely dependent on the basic pension.

Finally, the success of a saving pension scheme can only be achieved if incomes in the country are relatively high, income inequality is moderate, and employment is stable.

While in cases of high inequality, it would be possible to accumulate sufficient amounts of money by retirement if incomes were generally high in the country, but this is not the case in Georgia.

And Georgia has one of the highest levels of inequality in the region, with the wages of almost 80% of employees in Georgia are under ₾1,500 ($560). Income is concentrated in the hands of the few, which makes the saving system meaningless for the majority.

Since an individual saving scheme is based on the principle of self-care and does not contain any kind of redistribution mechanism, it will only reproduce and deepen existing inequality in old age.

There is an alternative

Criticism of the reforms would be unfair if a working alternative didn’t exist, but the fact is, there is an alternative that works almost all over the world as the main pillar of many pension systems. The pay-as-you-go (PAYG) system is based on the principle of solidarity between generations.

For this type of pension system, after employees participating in the scheme retire, their pensions (according to their merit and experience) are financed by the active workforce at that moment. That active workforce, when they retire, will then be financed by the next generation of employees.

This kind of system would have many advantages for Georgia. It could cover the thousands of people that will be left out of the government’s saving scheme, and significantly increase their pensions.

Such a system could possibly increase pensions instantly for new pensioners (already from 2020) and by a significant amount.

This is because the key to financing the PAYG system is not savings (which take time to accumulate) but the ratio of current workers to pensioners in the scheme.

There would be a big difference between the number of contributors (total number of employed), and the beneficiaries (those now employed who will retire in 2020 when there will be money in the fund), which is why the scheme could fully cover employees retiring in the near future and offer them significantly more than the private savings pension scheme.

Since the number of years someone has been enrolled in a PAYG scheme is one of the main determining factors in their final pension amount, for initial generations, this amount would be low. But a bonus system could be introduced in the beginning to offset this. Because there would be such a big difference between contributors and beneficiaries in the beginning, a huge amount of money would be accumulated which could be used to cover this bonus for the first generations of retires.

Unlike a private saving system, a scheme based on the solidarity principle could also provide some redistribution between different income groups, to alleviate elderly poverty.

[Read on OC Media: ‘People’s goodwill is my only hope for survival’ — elderly poverty in Georgia]

This scheme would provide pensions till the end of life, redistribution between different income groups, and a bonus system for new retirees. This could also act as a great stimulus for people to formalise their labour, as the promised guarantee of a decent pension on retirement could tempt many.

What a PAYG pensions system could look like, based on research — ‘The alternative vision of pension reform of Georgia: solidarity, sustainability and high benefit’ conducted by Center for Social Studies

No Inclusive growth without redistribution

The pension reform did not have public legitimacy, more than half of the population knew nothing about it, and it is a fact that this system needs at least 10 or 15 years to yield reasonable returns, thus thousands of citizens retiring in the coming years will still live in risk of poverty. This without mentioning those who will never sign up for the scheme.

While pioneering this reform, it is strange that the government has announced ‘inclusive growth’ as a priority, meaning that everyone, and not just a few individuals, should enjoy economic growth.

In practice, aiming for inclusive growth should mean the government actively pursuing some form of income redistribution.

The existence of a pension system with the private saving principle at its heart contradicts the principles of inclusiveness, solidarity, and redistribution that are the basis of the social state defined by our Constitution.

A pension system without mechanisms to cope with income inequality will only reproduce and deepen inequality in older age.

The Social Democrats faction in parliament, of which I am a supporter, will soon register a law to introduce a PAYG pension scheme as the main pillar of Georgia’s pension system. Presumably, discussions on pension reform will continue, but changes cannot be expected without public engagement.

Tornike Chivadze is an editor and blogger of analytical media portal European.ge. He is currently a researcher in the study funded by the Friedrich Ebert Foundation: ‘The alternative vision of pension reform of Georgia: solidarity, sustainability and high benefit’.

This article was prepared with support from the Friedrich-Ebert-Stiftung (FES) Regional Office in the South Caucasus. All opinions expressed are the author’s alone, and do not necessarily reflect the views of FES or OC Media.